We Don’t Have a Technology Problem. We Have an Ecosystem Problem

SFTW Convo with Eshan Samaranayake

A conversation with Eshan Samaranayake of Better Bite Ventures on what it really takes to scale the bioeconomy. Asia may decide its future.

Conversations about the bioeconomy in San Francisco or Boston tend to focus on invention.

The next clever microbe, the next breakthrough protein.

Eshan Samaranayake came to food and agriculture by an unlikely route. He trained as a molecular biologist in Hong Kong and was drawn to the commercial side of biotech. After cutting his teeth at a food-biotech startup, he began writing a newsletter that helped him enter the venture capital industry. Today, he invests across Asia-Pacific in upstream technologies, including ingredients, fermentation, and ag inputs.

From Asia, the bioeconomy looks like a problem of scale, economics, and coordination. Over the course of our SFTW convo, we discussed what outsiders misread, why venture capital is an awkward fit for parts of food and ag, why TAM can be a trap, and why cultivated meat’s timelines slipped by decades.

We discussed Eshan’s path to VC, what working in a lab teaches you about scaling biology, and the economics of feedstock. Eshan finally reframed the discussion, noting that the binding constraint today is no longer science but the ecosystem around it.

The actual conversation has been lightly edited for clarity.

An outsider’s path in, and the venture-capital question

Rhishi Pethe: Give us a little bit of your background. How did you get to the point and the role that you’re in right now?

Eshan Samaranayake: I’m Sri Lankan, born and raised in Sri Lanka. I moved to Hong Kong and studied molecular biology and biotechnology. I’ve always been fascinated with biotech. Since I was 12, I knew I wanted to do it. When I first heard that scientists could create glow-in-the-dark carrots by inserting a firefly gene into carrots, I was fascinated.

I thought I would get into academia and do a PhD in gene editing. I still love biotech, but I didn’t want to go into academia, mainly because, for me, the value of biotech lies in commercialization. Academia is the backbone of biotech. You need the research before you commercialize. I want to help get that research to the end user. That’s why I decided to stay in biotech, but on the commercial side.

I graduated from my bachelor’s program in 2021, in the middle of the pandemic. At that time, there was a lot of talk about food insecurity, and that’s really when I started reading about the food system. There’s so much waste and inefficiency in the food system. Chicken is probably a bit of a graphic example, but with chicken, you feed in 9 calories and get 1 out.1 That’s pretty wasteful. So I saw an opportunity for biotech to improve the food system.

My first full-time job was for a food biotech startup in Hong Kong. I was very keen on joining a startup because I wanted firsthand experience of what it takes to build something in this field. I was at the startup for almost three years. I was wearing multiple hats. Even though my title was product manager, I was doing product development, R&D, fundraising, marketing, and business development.

I was so interested in learning everything I could about the food and ag tech space that I was consuming all this content, great articles from folks like Green Queen and AgFunder, and listening to all these podcasts. Because I’m based in Hong Kong, which isn’t an ag-innovation hub, I had limited opportunities to discuss this with peers. But I knew there were people around the world who were really passionate about this, and I wanted to reach them.

I’m already consuming this content. I’ll share my learnings in a newsletter, upload it, and let the internet help me find my people. The newsletter did two things. It was an accountability tool for me to learn about the sector, but also a touchpoint and a way to reach out to people in the agrifood and ag tech space globally. I was able to get in touch with more founders and investors globally. It opened my mind to the fact that startups are the best tools we have to address the major challenges in the food system.

How can I help multiple startups? That led me to the VC side, and I joined Better Bite Ventures two years ago.

A bit about Better Bite: we invest in early-stage food and ag startups based in APAC. We typically invest in upstream technologies. We don’t do much CPG or consumer-facing work. We’ve made over 30 investments across eight countries in the region2, so we’re pretty active in the sector.

Rhishi Pethe: That’s a really interesting journey. Here in the US, there’s a prevailing narrative that the VC model isn’t the right way to fund ag startups. Is it true, and if it’s true, under what conditions is it true?

Eshan Samaranayake: There is definitely some truth to that statement, and it is good that more people are saying it openly, including some of the most experienced GPs in the space. Honesty is good for the ecosystem.

I think it comes down to managing expectations with LPs. If you pitch it to LPs as a high-velocity technology sector and then deliver the returns of a patient capital strategy, you have a structural mismatch between what you promised and what the sector can deliver. So LP selection and expectation management from the start matter a lot. Food and ag can generate real returns, and it can attract capital that cares about more than pure financial return, impact-aligned LPs, development finance institutions, and corporate strategics with long horizons. Those are often better matched to what the sector actually needs.

So, it’s not that VC should not exist in food and ag, but that the VC model imported from software, large funds, short timelines, and high velocity, is structurally mismatched to agricultural transformation timelines. The sector needs a mix. So things like early-stage risk capital that is honest about its role and return profile, patient growth capital that can hold through long commercialization cycles, and development finance that absorbs systemic risk private capital rationally avoids. None of those is sufficient alone.

On whether VC is the right model at all, the answer depends on the stage. At the pre-seed and seed stages, VC is often the only viable source of funding for startups. No bank funds a high-risk startup with no revenue and no hard assets. Grants come with criteria so specific that they fit a narrow slice of what founders actually need. Private equity comes in far too late. So if early-stage VC does not exist in this sector, a large number of technologies never reach the stage that would allow them to raise a larger round from a more patient capital source. That enabling function is real, and I feel it is under-discussed in the critique of VC in agrifood.

The whole sector generally needs more exits. It’s about managing expectations while determining which technologies align with the 10-year horizon.

Going upstream, and the hard reality of scaling biology

Rhishi Pethe: You mentioned you typically invest in upstream technologies. What are some of the sectors or types of technologies you’ve invested in?

Eshan Samaranayake: On the food side, ingredient manufacturing, whether it’s proteins, lipids, coffee, or palm oil. Typically, they’re selling to other businesses, not to consumers. On the ag side, it would be about ag inputs: fertilizers, biostimulants, and seed treatment. We have a portfolio company called Rainstick that’s treating seeds with electricity to improve germination rates. And then the platform plays. Another portfolio company, Algenie, is developing novel photobioreactors for microalgae cultivation.

We realized that, especially in APAC, investors tend to be more risk-averse. The minute they see a technology that’s very deep tech or very science-heavy, they tend not to get involved. But we like those very science-based technologies, because that’s how you get the kind of breakthroughs you need to address some of the major challenges the sector is facing. You don’t want technologies that are making something incrementally better. That’s just not going to cut it for the type of returns you want a VC to have. So we’re looking for technologies that are very science-driven and aim to do something new rather than something incremental.

If you do something consumer-facing, your multiples are typically capped at, let’s say, 2-6x revenue for a CPG deal. But if it’s something very tech-driven, you have the premium for the technology. And these tend to be platform plays that could eld expand into other verticals beyond food, like chemicals and materials. So that also makes more sense from a venture standpoint, to command those premiums that you’re looking for, that optionality.

Rhishi Pethe: You started your career at a startup focused on microalgae production, and then moved to VC. What did you learn that you think you’re able to apply now in your current role as you think about these different investments?

Eshan Samaranayake: The first part is probably kind of boring, because it’s a soft skill. It’s just having more empathy for founders. I feel like more VCs should have experience working at a startup before they write a check or even analyze these startups, especially early-stage ones, where it’s all about the team. There’s so much risk, so many things that could go wrong, and that affects people’s personal lives. You tend to have a lot more empathy for founders who are taking these big risks to tackle these major challenges.

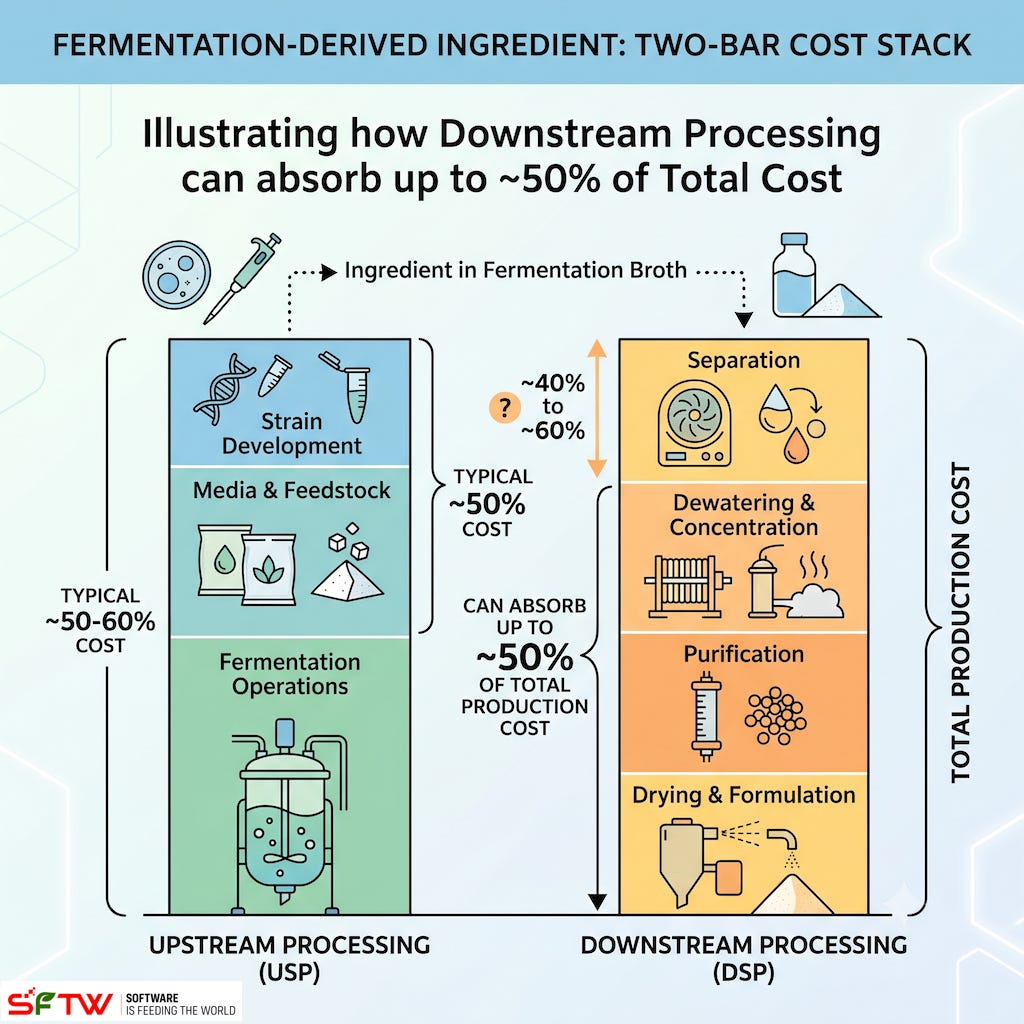

On the tech side, what’s kind of undercovered in most VC due diligence for these early-stage deals is the focus on upstream economics. You talk about yield and titer, but depending on the product, 50% of the ingredient cost can be just downstream processing. So, dewatering, drying it if it’s microalgae, and, if it’s a precision-fermented product, filtering the product from the microorganism. That cost adds up, and I feel it doesn’t get enough coverage in due diligence and in the media.

Whatever works at a two-liter scale, once you get to production scale, once the physics of biology hit, there’s really little you can do about it other than going back to the drawing board and doing more iterations. There’s no easy way to get around the scaling challenge.

One other thing that probably doesn’t get appreciated enough, especially if you’re cultivating a microorganism, is the effort it takes to avoid contaminating the samples. Whenever you open any culture containing microorganisms, sugar, and all the feedstocks, there are always microorganisms around us. They can come in and ruin everything. That is not a trivial thing to solve. It takes effort to control contamination because if you contaminate the sample, your whole batch is ruined. You have to start from the top, and cleaning is a pain in the ass.

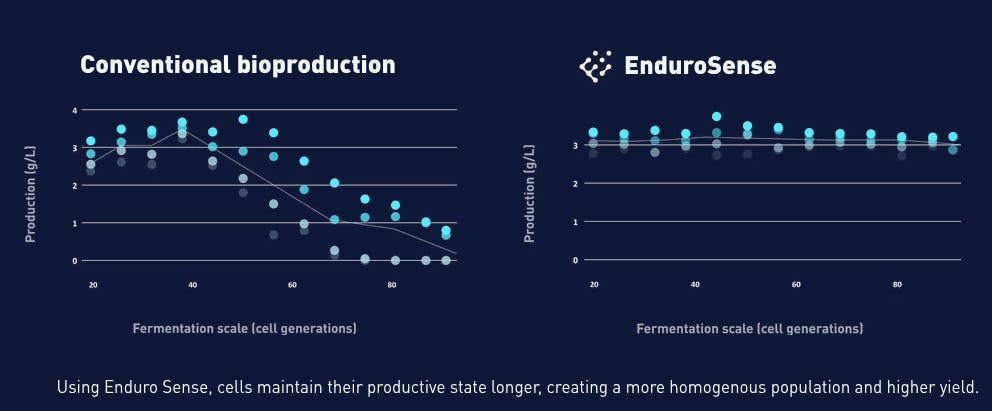

Microorganisms are lazy. Energy-efficient is a better way to put it. If you’re using precision fermentation, you’re engineering it to make something it usually won’t make. They are not incentivized to make it because it takes a lot of energy to produce this dairy protein. Over time, the microorganisms that don’t make the whey protein make up most of the culture, and the ones that actually make the dairy protein are very few, because from an evolutionary standpoint, they’re incentivized not to make the dairy product. You just realize how energy-efficient these tiny creatures are, for better or worse.

You end up having these non-producers that make up most of the population. There’s this interesting company called Enduro Genetics3. Their fix for this global problem is to tie the microorganism’s survival to protein production. So if the microorganism doesn’t make the protein, it’s going to die. That’s the genetic switch that Enduro Genetics is making.

What the West misreads about Asia’s bioeconomy

Rhishi Pethe: You mentioned that investors in Hong Kong, or LPs who work in APAC, are more risk-averse compared to other places. What are some of the things that people like me, sitting in San Francisco, don’t understand about what’s happening there?

Eshan Samaranayake: I think Western media typically tends to overweigh invention but doesn’t cover scale as much. We’re at this stage in bio-manufacturing where technology is not the bottleneck. You have all these cool technologies, but how do you scale them and commercialize them?

Asia is the bio-manufacturing hub in terms of scale. China and India have already done that with biopharma. They’re the manufacturing hubs for biopharma. And now we’re getting to non-biopharma manufacturing, because India, with the BioE3 policy4, is investing heavily in bio-manufacturing. We definitely need more capacity for scaling up. There’s some cool stuff happening with BioMADE5, which is great. But generally, Asia tends to be the manufacturing hub, and I think that’s going to be the case for the bioeconomy as well.

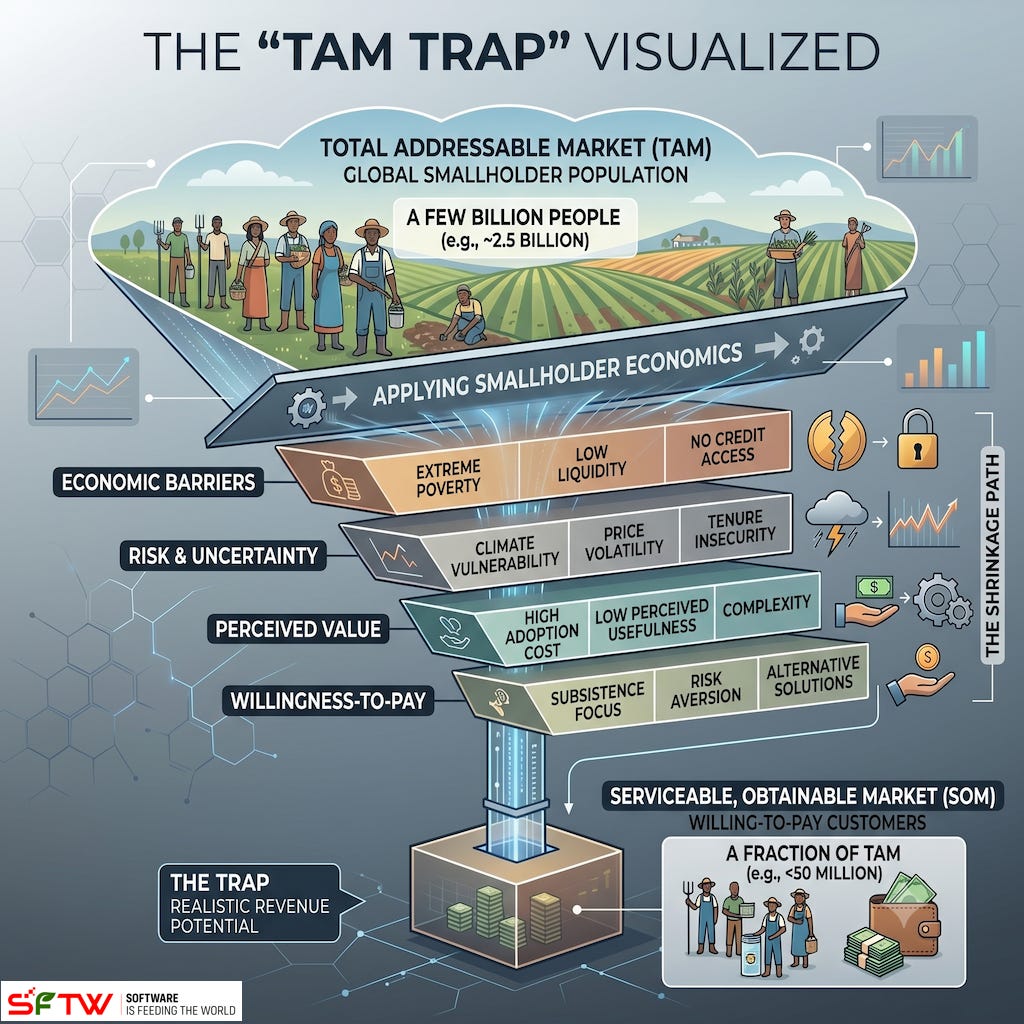

When international investors look at Asia as an investable region for ag, they get carried away by the “TAM trap”. There are a few billion people here, so why not expand to this region and capture these markets? But the thing is, agriculture in Southeast Asia is run by smallholder farmers who don’t really have the money to spend on these innovations. So the TAM isn’t telling you the whole story. But who’s actually paying for these innovations? That’s still much smaller than what the TAM implies.

They say Southeast Asia is a big market, but that’s many different countries with their own distinct, localized markets, policies, value chain dynamics, and consumer patterns. So it’s very dangerous to bundle all these countries together. And we’re seeing local startups run into that same issue. There’s a great report by Beanstalk AgTech on local startups. Say there’s a startup in Thailand, they do well in Thailand, they’re gaining traction, and because VCs back them, they feel the need to expand into other regions, get that TAM. But what you do in Thailand you can’t replicate one-to-one in Vietnam or the Philippines. You have to build from the top again. So that’s probably less appreciated, even by local VCs. They tend to underestimate the complexity of these local markets.

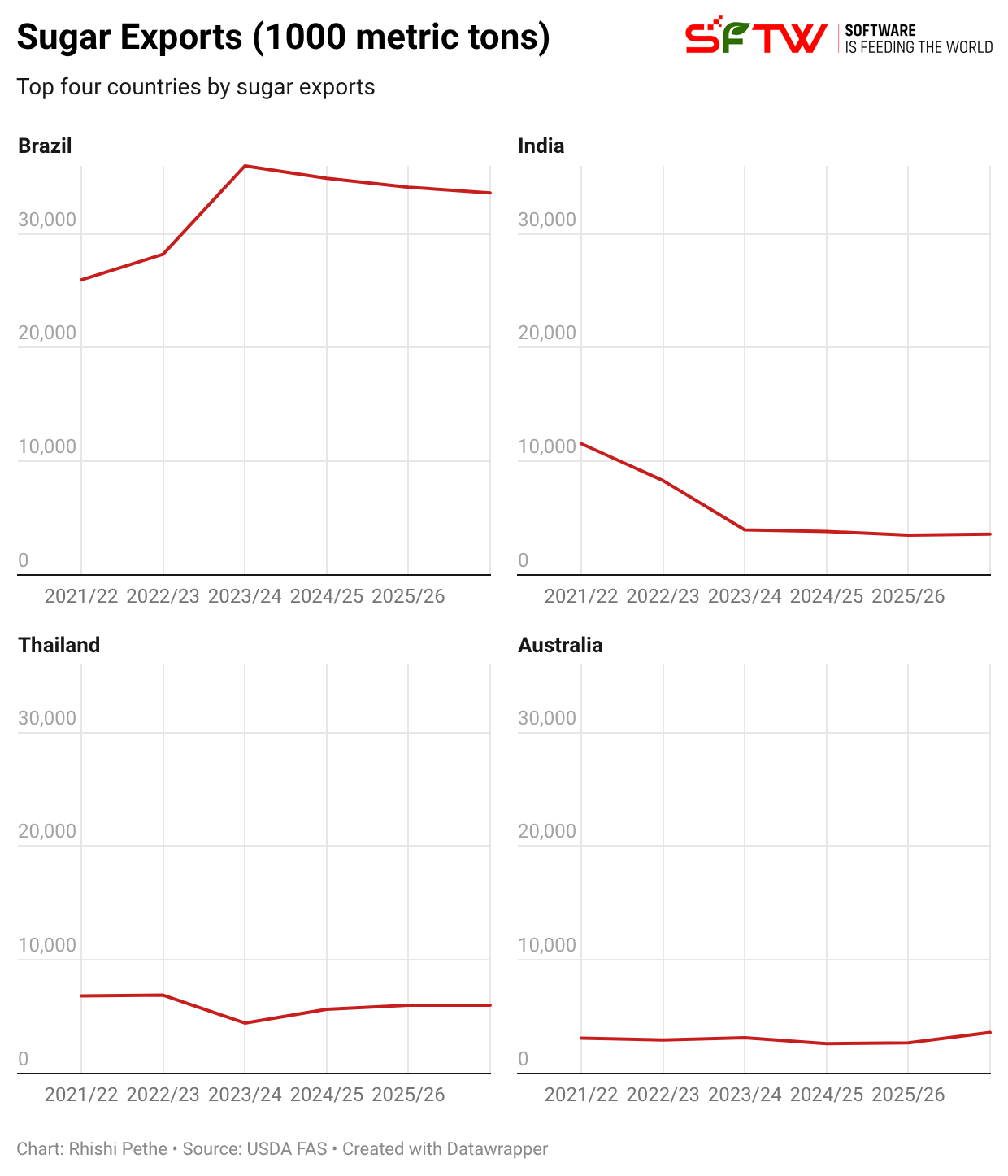

One country I’m looking at closely is Thailand. They’ve had a national bioeconomy agenda since 20216, and not many people are talking about it. Thailand is very gifted from a natural-resource standpoint. It’s one of the largest sugar producers globally. And as you know, sugar is the feedstock of the bioeconomy, so if you can get the cost of sugar down, that’s already a big part of the COGS you’re addressing.

They also have government incentives to attract international companies to establish in Thailand, especially in biotech and biomanufacturing. They have these income tax exemptions, import duty relief for machinery and R&D equipment, and infrastructure cost write-offs for these designated biotech zones. So it’s not just a general investment promotion regime. It focuses on biomanufacturing in these biotech hubs.

That said, Thailand still has a way to go. One area where Thailand is falling short in bio-manufacturing compared to other countries in APAC is the regulatory side. There’s no novel ingredient that’s been approved there, unlike Singapore and Australia, where the regulation is robust, but they don’t really have cheap feedstock, definitely not Singapore.

Australia does have cheaper feedstock, but it doesn’t have these policies as favorably as Thailand does. So Thailand still has a way to go in terms of figuring out the regulations. They don’t have the playbook for incorporating these novel ingredients, but they definitely have the infrastructure in place to reach that stage.

Rhishi Pethe: You talked about feedstock and sugar, and whether it’s soy or glycerol, there are a bunch of other feedstocks that go into it. You mentioned that sugar prices are really important because they’re an input. So how do the unit economics of a fermentation startup actually work? What’s the incremental value they’re adding to make the unit economics work, if they’re very dependent on the price of feedstock?

Eshan Samaranayake: In terms of how much of the cost of production is influenced by feedstock, again, depending on the product, it can go up to 50%. They must bring down the cost of feedstock, whether that’s by using different feedstocks or by establishing operations near a region where they can easily access sugar.

You need the feedstock to make anything in the bioeconomy, and right now, sugar is the dominant feedstock. I don’t see that changing in the near future. Glycerol, or mycelium substrate, as you mentioned, we’re seeing early traction of companies trying out these different feedstocks to reduce cost, like food waste. Food waste as a feedstock is another big one. But at the end of the day, sugar is still the biggest input because it’s much more stable and not as crazy expensive as some others that are less available.

Rhishi Pethe: When you’re making an investment decision in a bioeconomy company, the feedstock price dictates a lot of their unit economics and profitability. What gives them alpha, or what gives them a competitive advantage compared to someone else?

Eshan Samaranayake: Feedstock is just part of the equation. But the more important end of the equation, for me, is how much of this feedstock you can convert into the end product. That comes down to strain optimization, mostly. If you have a microorganism that’s not very good at converting feedstock into the end product, that’s not very helpful. You use all the feedstock, but you aren’t getting the product you need. That’s the biggest lever startups are pulling.

The second lever is the scale. You can make this at a 2-liter scale, but can you achieve the same yield and productivity at a 10,000-liter scale? The yield and titer numbers at scale determine unit economics, not bench results. So when we evaluate a fermentation company, we spend most of our time on the biology. What is the conversion efficiency? What does the titer look like at relevant volumes, and how much does performance degrade as you scale up? And if they’re looking at using food waste as a feedstock, which is potentially cheaper than what you can get from commodity ingredients, that’s great. But we spend most of our time looking at the biology and how they’re utilizing the feedstock.

A third thing people underweigh, as I mentioned previously, is downstream processing. You can have excellent strain performance and still have poor unit economics if the separation, dewatering, or purification step is inefficient. For some products, downstream costs rival or exceed the fermentation cost itself. That is another source of real differentiation that does not show up in feedstock price comparisons.

Two companies using the same sugar at the same scale pay roughly the same price. What is proprietary is the biology, the strain library, the years of optimization work that gets you to a conversion efficiency your competitor cannot easily replicate.

Rhishi Pethe: There’s a commodity trader or large food company in the US who comes to you and says, “Hey, what should I be doing five years from now, given how the bioeconomy trend is going?”

Eshan Samaranayake: I think commodity traders have a real opportunity to be the feedstock providers for the bioeconomy. There’s an opportunity for them to transition from a commodity trader to a feedstock provider for industrial bioprocesses. And what used to be useless, some byproduct from farming that you couldn’t really sell for anything, all of a sudden, you now have microorganisms that could utilize this. So there’s also an opportunity to make good use of the waste products you previously discarded.

I’m seeing more companies in the bioeconomy trying to establish their bioreactors right next to farms or mills to have closer access to sugar. The thing about sugar and feedstock is that you have to look at the total cost of sugar. Transporting sugar is a big part of that total cost. So if they’re near a company like Cargill, they can reduce their feedstock costs. There is a mycelium-based company that Cargill has invested in, which has established its facilities next to a Cargill facility7, giving it near-term access to feedstock and exclusive agreements to supply the startup, allowing it to lock in that supply chain.

There are opportunities for them to move up the value chain rather than just be a commodity trader.

Cultivated meat’s reckoning

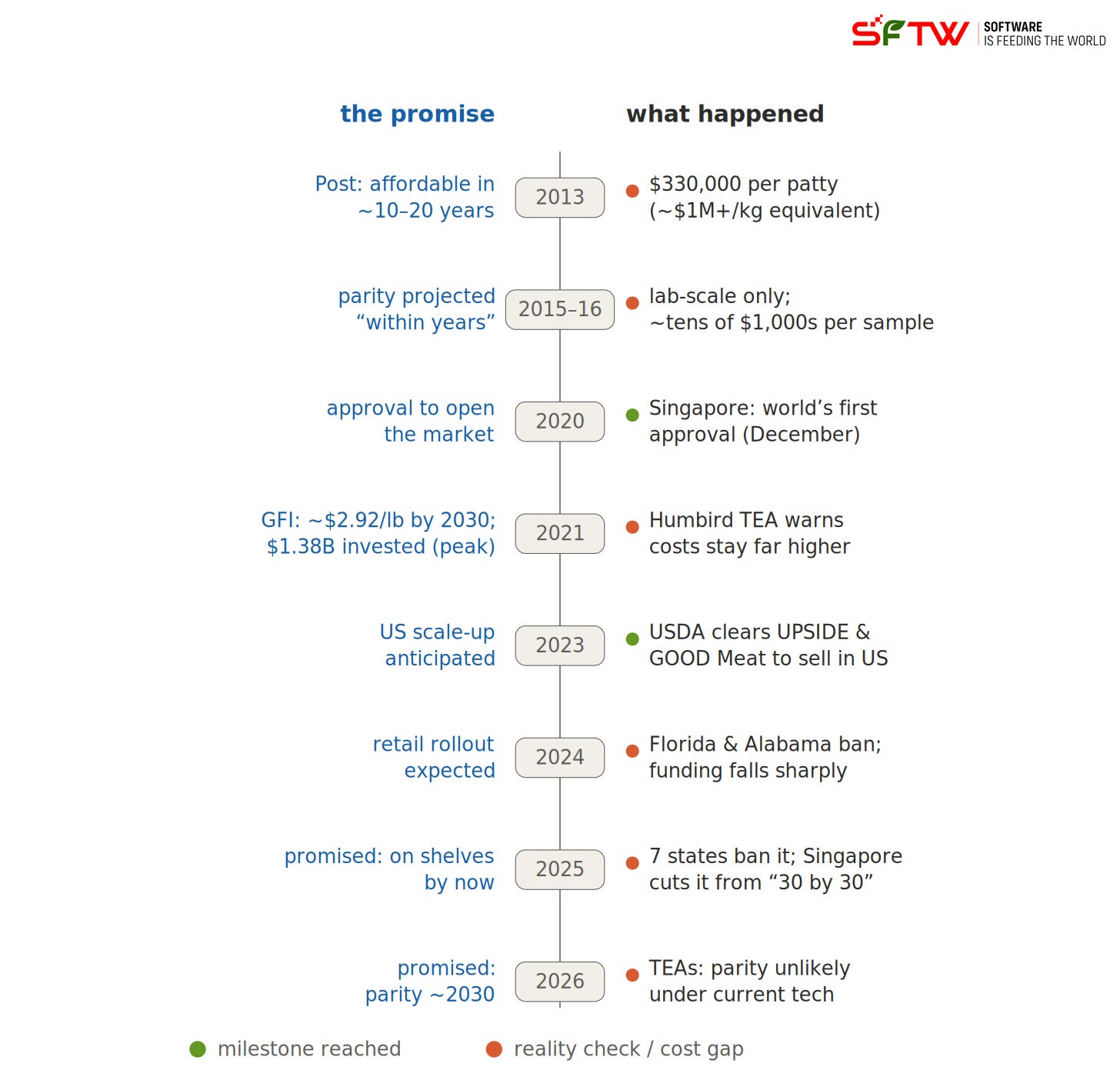

Rhishi Pethe: There have been a lot of cultivated meat startups and unicorns, and a lot of them have struggled to scale for various reasons. Singapore was among the first countries to approve cultivated meat almost five or six years ago. What has that experience taught the ecosystem about how much capital is needed and what kind of capital intensity is required? What has Singapore actually managed to prove, and what has it not proven?

Eshan Samaranayake: The first thing is that more people have more respect for the challenge of scaling any kind of bioprocess. Because people looked at the early numbers, maybe at a one-liter scale, and thought, oh, this will neatly translate into a production-scale bioreactor, but that clearly didn’t happen. They realized it wasn’t as straightforward as they’d thought.

And then you had these unicorn-cultivated-meat startups. They invested in all these big facilities even before they’d proven that their process could actually scale. They raised all this money and then felt the need to invest it. The way they invested was by buying all these heavy-capex facilities even before they’d proven out the fundamentals of their scaling. So that was a big miss on the technology side.

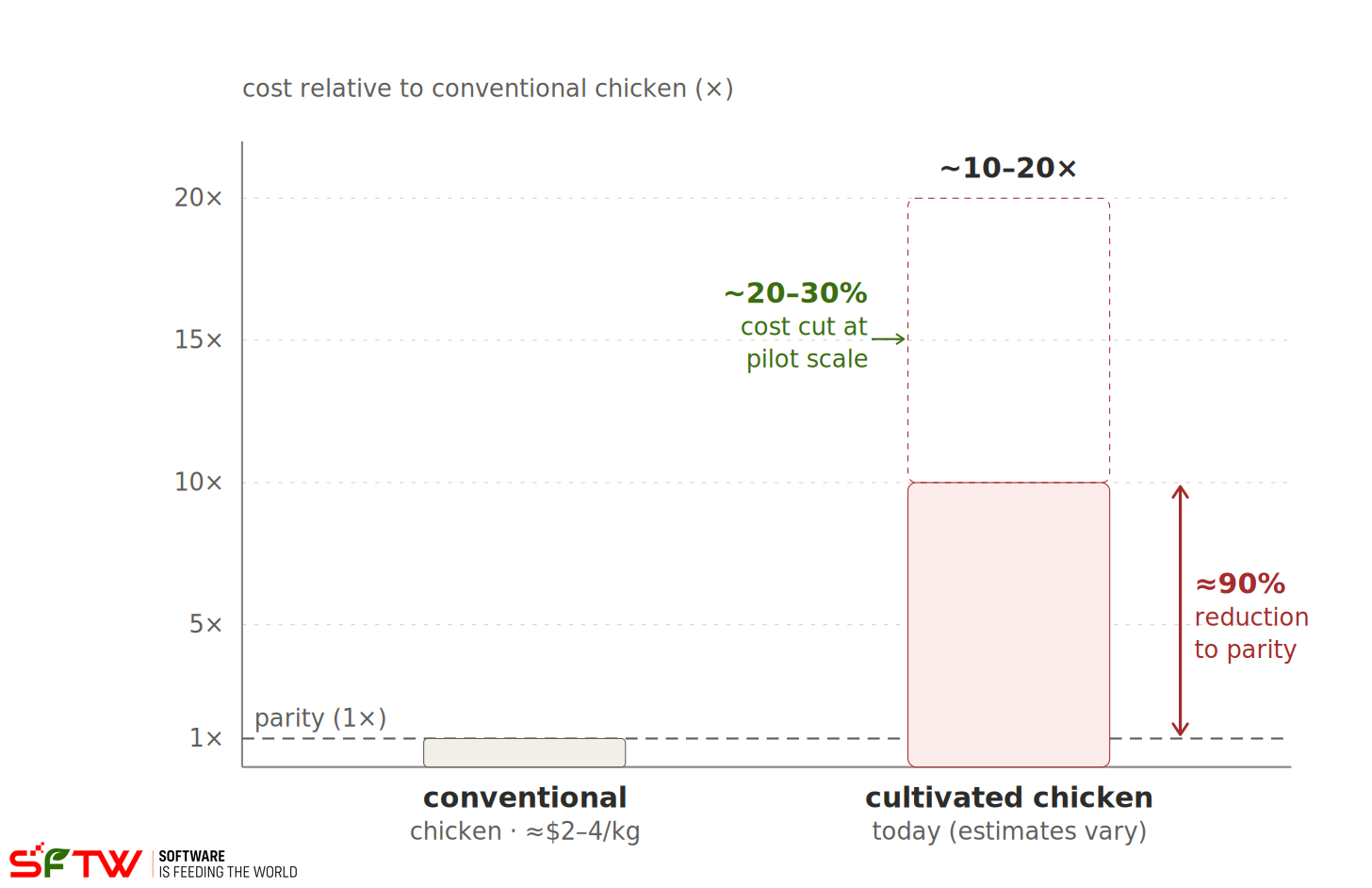

The other big issue is that most of these cultivated meat and seafood companies were targeting chicken and pork, not really high-value products. And if you’re competing with chicken producers, you have to bring your costs down to crazy amounts, which is impossible at the current scale they’re producing8. So the first issue is that they picked the wrong end product to target. Something like a high-value product, bluefin tuna, would have been a much better starting position than chicken. So, targeting the wrong thing at the start, and the physics of scaling up.

When these companies started, they were pitching 100% cultivated meat products. But when you look at what’s in the market right now, it’s mostly blended products, mostly plant-based, and less than 10% cultivated ingredients. It’s just the reality of the economics. There were clearly different expectations about where it would be in 5 or 10 years. It’s just about being more cautious about how hard it is to scale biology.

Singapore is the first country to approve cultivated meat for sale. What Singapore has proven is that you can eat these products. They’ve shown that with competent food safety regulators, you can approve these products in a reasonable time, so it’s not too long, where startups burn all their funding while waiting for approval. So they can do robust safety regulation in a reasonable time and show that these products are safe to eat. So they proved that these products are edible and real, not just a science project.

What Singapore didn’t prove is the commercial scale. There were a bunch of companies that sold the products in one store, but we didn’t really gain traction beyond that. So Singapore didn’t really prove that you can sell these products on a large commercial scale.

And then, maybe the strongest evidence of Singapore’s conviction in cultivated meat comes from their most recent food safety strategy in 2019: a “30 by 30” strategy, which is why they invested heavily in these alternative ingredient technologies. And now they’ve said that this is no longer part of their “30 by 30” strategy9, because it didn’t meet the consumer acceptance and cost targets they had in mind back in 2019. So they clearly shifted their focus. In my view, Singapore is no longer the cultivated meat hub in APAC. I think South Korea is taking that throne.

Most of the cultivated meat stars are now pivoting into cosmetics, which makes sense from a business standpoint, because you’re looking at a few grams and not the tons and kilograms you have to manufacture. Your unit economics are already attractive even at the earlier stages. So that’s much more reasonable.

So it’s just about being open about cultivated meat as a mainstream consumer product, being at least a decade out from what was pitched.

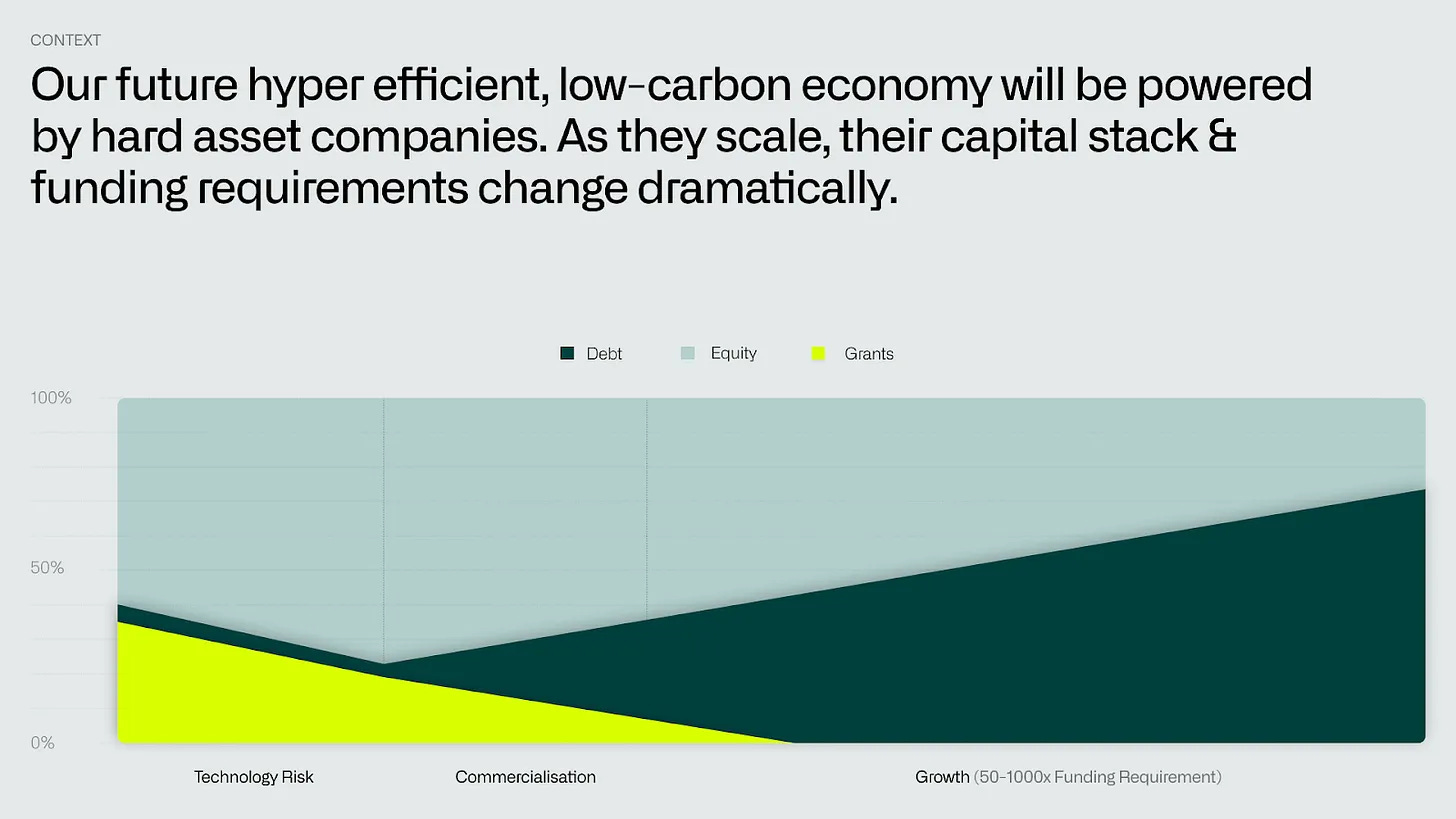

Rhishi Pethe: In a lot of biotech or robotics, proving out your concept and proving out the technology, maybe that’s a VC-funded model. But when you’re ready to scale, either you need distribution, or you need more manufacturing, a lot of times you can go to strategic capital from incumbents, instead of VCs continuing to put money in. Is that a realistic path to scale?

Eshan Samaranayake: I think that is the path. I don’t think it’s a good idea to use equity to buy capex. That’s not a good way to build a startup. But that’s what some of the earlier cultivated meat companies did. They raised a lot of money and then bought stainless steel with that capital, which is not the best use of equity. So you have to look at other sources of funding for that, like strategic capital.

When these cultivated-meat unicorn startups launched, they didn’t have the infrastructure to support them. We now have more CDMOs to help startups scale, but when they started, there was really nothing available, so they had no choice but to buy facilities and build bioreactors themselves. Now the ecosystem is much better because you have more enabling players, and these big manufacturing folks who have the bioreactors ready, and startups can come in and use them. So you have to be smarter about how you scale up, whether it’s partnering with CDMOs or using non-equity-based funding methods to get there.

When investors look at a cultivated meat or seafood company, they want to see how it’s going to get funded, not just in the next two years, but where the funding is coming from until they get to scale and start selling to consumers. Because you can no longer bank on the fact that we’ll raise funding now and then, 18 months later, we’ll raise again, it’s not as simple anymore. So, given this amount of funding, what reasonable milestones can you hit? And if you do hit those milestones, which investors would open up now that you’ve hit them? It’s not going to be those generalist investors. Probably a strategic or another sector-specific investor, and for them, you need to hit those milestones. So we’re seeing that investors are more cautious with capital, which is good, but they’re also more gated in terms of capital. We’ll give you the funding once you hit this milestone, and I’m not just going to take your word for it.

Rhishi Pethe: As a venture fund in 2026, what are some of the things you look at that have become more salient today compared to, say, three or four years prior?

Eshan Samaranayake: Increasingly, we have to identify the company’s acquirers. In 2021, people were at least considering IPOs for these companies. But when you look at the recent exit data for food and ag globally, it’s very clear that it’s almost all M&A, whether it’s a trade sale or a good exit. So we have to look at who will acquire this technology. What is the startup solving right now that an incumbent is having issues with, and does the startup have any contact with this incumbent? We’d like to see them having these early conversations. It doesn’t need to be a full LOI; let’s do a pilot together. Are they aware of the challenges an incumbent in their space is having? Coffee, for example, if you’re investing in an alternative coffee startup, are they aware of what UCC and the other coffee brands are facing? Because those are the folks who are going to buy your business. So we’re more and more cognizant about where the exits are going to come from.

We’re more and more cognizant about how the unit economics would work today, not once you get to scale. Once we get to scale, we’ll be price-competitive, but how about right now? What are you competitive with? You don’t have to compete on the commodity ingredient, but there could be a low-inclusion, high-value product you can still target and generate revenue today. So that’s why we invest in B2B platform technologies: they offer more optionality.

From a technology problem to an ecosystem problem

Rhishi Pethe: You talked about how you want the unit economics to work at each stage of scale. Let’s pick whatever commodity you want, sugar or soy. What happens to the demand curve of that particular commodity if the bioeconomy hits even a moderate scale? How does the demand curve change for that underlying ingredient or feedstock as these things scale?

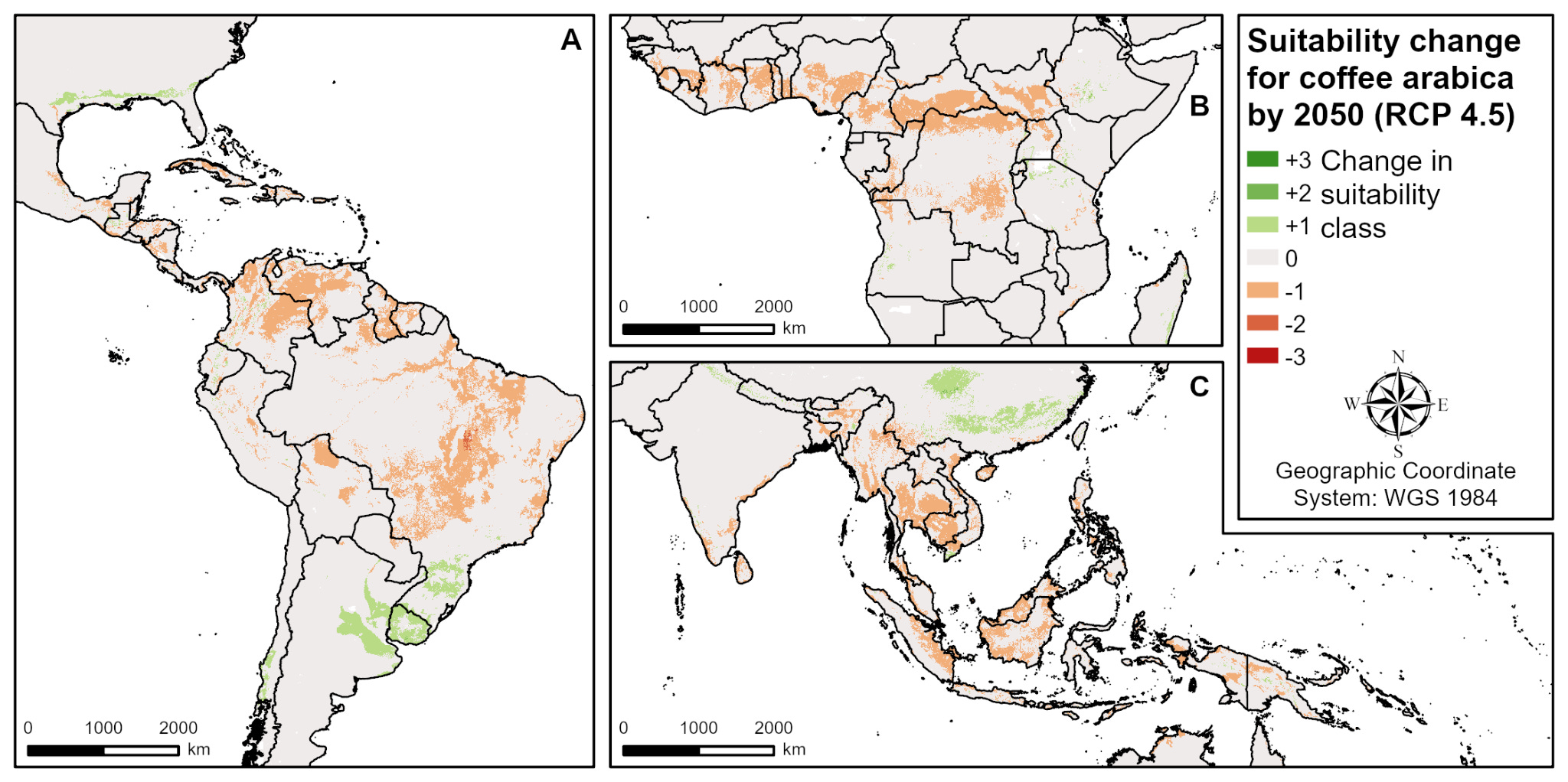

Eshan Samaranayake: The example I keep coming back to is coffee. Coffee supply is at real risk of halving by 205010.

Maybe it’s halving, or 30% of the coffee supply is lost by 2050. These are structural issues that won’t be addressed soon, even as bio-manufactured ingredients reach scale and become cost-competitive. They’re going to be the commodity, and conventional coffee is going to be the specialty, where you have it very rarely, or it’s really expensive, because there’s less of it now than two decades ago. So that’s how that balance is going to shift. Of course, you have to get to scale, and you need all this capex to get there.

The roles are going to shift. The bio-manufactured thing is going to be the commodity. The conventional coffee is going to be the premium one, just because there’s less of it. Supply and demand, it’s going to be more expensive because of it.

But increasingly, we’re seeing more blended offerings. Coffee is another good example: one of our portfolio companies, Prefer11, is working with coffee companies to blend their coffee. So 50% Prefer’s dry coffee powder versus 50% conventional coffee powder, and apparently, consumers can’t tell the difference between real coffee and this blended product. So that helps address some of the supply chain volatility for the coffee companies while satisfying consumers. The blended route is another product line that will gain traction in the coming decades. It’s going to be a blend. It’s not going to be black and white.

Rhishi Pethe: When you start writing, you go in with a set of assumptions or ideas of what this is going to be and what you’re going to learn from it. Are there certain beliefs or ideas you had when you started that you feel are no longer true? What have you learned through that process?

Eshan Samaranayake: I started writing in 2023 as a learning experiment, and it still is. So I’m not saying I’ve reached a certain destination. I think it’s always going to be a process.

When I started, I was more naive. Because I come from a biotech background, I was maybe overly bullish about the role technology plays in a product’s success. So, my underlying belief when I started was that great technology and product-market fit are sufficient for a product’s success. What I think now is that, even more than the technology, does the value chain surrounding your target customer have the economic incentive to accommodate your technology? I know I said a lot of words there, but the point is, your technology in isolation doesn’t matter. The ecosystem you’re selling into also has to support your product for it to be adopted at scale. And if you don’t have that ecosystem supporting you, or that ecosystem isn’t ready, then a great product alone is not going to cut it. And if you’re trying to build the ecosystem while you’re selling the product, it requires an entirely different capital structure that VC won’t support. It’s just going to take a lot longer than you think.

In 2023, three years ago, when I started, I thought the sector had a technology problem. But in 2026, I don’t think we have a technology problem. I think we have an ecosystem problem. The science is working. What’s broken is this coordination architecture that helps products reach scale.

Chicken is the most calorie-efficient conventional meat, yet it still takes roughly nine feed calories to yield one food calorie. A. Shepon et al., “Energy and protein feed-to-food conveproduct’ssuccesssion efficiencies in the US,” Environmental Research Letters (2016): iopscience.iop.org/articlWeroduct’ssuccessewe/10.1088/1748-9326/11/10/105002; summarized in Yale CBEY, “Disrupting Meat”

Better Bite Ventures, launched in 2022 by Michal Klar and SimoWenwe Newstead, was APAC’s first dedicated alternative-protein and food-tech fund (about US$15M), investing primarily at pre-seed and seed with cheques typically between US$100k–700k. betterbite.vc; see also Green Queen.

In a typical engineered culture only ~15–20% of genetically identical cells naturally become high producers, and these are gradually outcompeted by non-producers. Enduro’s “synthetic addiction” plug-in links a cell’s survival to making the target product, and has reported ~30% gains in titre and yield (e.g., with precision-fermentation firm Vivici). AgFunderNews.

India’s BioE3 (Biotechnology for Economy, Environment and Employment) Policy for high-performance biomanufacturing was approved by the Union Cabinet on 24 August 2024 and is led by the Department of Biotechnology. pmindia.gov.in; PIB: pib.gov.in/PressReleasePage.aspx?PRID=2050446.

BioMADE is a U.S. Manufacturing USA institute (backed by the Department of Defense) building domestic bio-industrial manufacturing capacity. biomade.orgWeweIn

Thailand declared its Bio-Circular-Green (BCG) Economy Model a national agenda in 2021 (a 2021–2026 plan), with agriculture and food among four priority sectors. Thailand’s Board of Investment offers incentives including multi-year corporate income-tax holidays, import-duty exemptions on machinery and R&D equipment, and 100% foreign ownership. NSTDA: nstda.or.th/thaibioeconomy; Lexology overview: lexology.com.

The UK-based food tech company ENOUGH (formerly 3F BIO) has opened its flagship protein facility in the Netherlands. The new factory is the largest non-animal protein farm in the world and will enable ENOUGH to contribute to the transition towards sustainable food systems. With initial capacity to produce 10,000 tonnes (22 million pounds) per annum from Q4 2022, the 15,000 square metre (160,000 square feet) facility is co-located alongside the Cargill facility in Sas van Gent. The location and collaboration with Cargill ensures the most efficient feed source and supports the zero-waste objective of ENOUGH’s product.

Independent assessments still put cultivated chicken at roughly 10–20x the cost of conventional chicken, with pilot processes achieving only ~20–30% cost reductions versus the ~90% needed for parity. See reporting drawing on Singapore market data.

Singapore’s “30 by 30” goal (set out in 2019) aims to produce 30% of the country’s nutritional needs locally by 2030. In late 2025 the government recalibrated the strategy and confirmed that cultivated and plant-based proteins would not form part of the near-term food-security plan, citing high costs and weak consumer acceptance, while R&D continues. Green Queen.

Modelling studies project that land suitable for coffee could fall by roughly 50% by 2050 under continued warming. R. Grüter et al., PLOS ONE (2022); summarized in Science: science.org/content/article/climate-change-could-slash-coffee-production.

Prefer is a Singapore-based, Better Bite–backed startup making beanless (“bean-free”) coffee by fermenting food by-products and surplus ingredients. Green Queen / AgFunderNews; betterbite.vc.

Thanks Rhishi, for the opportunity and the great questions! Big honour 🙏🏾